What happens to our money when it is not used? They lose their value. This problem consists of two components:

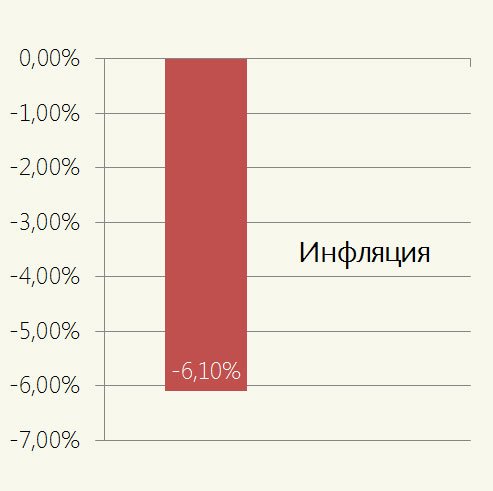

1) Inflation in Russia in 2011 was 6.1%. According to the results of 2012, they promise inflation in the range of 7%. I am not talking now about "personal inflation", which is individual for everyone.

Personal inflation is essentially an increase in the prices of goods/services that you buy. For example, you only buy gasoline, but you don't buy food. In this case, your inflation will be a % increase in the price of gasoline, without affecting other products. In this case, 5.59% if you drive 92m (based on gasoline prices on average in the country). If you buy not only gasoline, then your personal inflation will consist of an increase in the prices of all goods that fall into your consumer basket. And it is by no means a fact that it will be equal to the national average.

Inflation has both positive and negative sides for the country's economy. For us, every percentage of inflation means that with our money we can buy a percentage less goods and joys. In our case – 6.1% less joys or sweets:

By the way! Is your salary indexed according to the inflation rate at work? If not, it means that every year you get less and less…

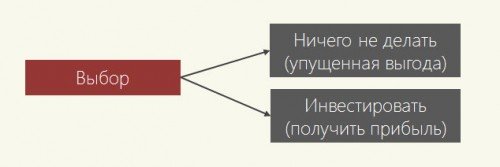

2) The lost profit is more abstract. It means that at each unit of time you have a choice:

According to Wikipedia, lost profits are unrealized opportunities to generate income, profit due to an unsuccessful choice of an image, a method of action.

So, in business, lost profits are equated with direct losses. Why should we think otherwise?

How much do we lose? The deposit rate in banks ranges from 5-6% to 12%/per annum. This is the amount of profit that we lose by simply keeping money at home.

Let's take the average rate of 7%. What happens at the output?

There is no end to the sadness. Thanks to our inactivity, we lose at least 13% per year of the amount of carefully accumulated savings.

Conclusion: "Keep money in a savings bank" ©. Or invest. Invest money at least on a deposit that will cover % of inflation. In this case, your losses will already be equal to 0%. Pay off your loans or try other ways of investing (we'll talk about them later). Every % won back from inflation or our inaction is your investment in future wealth.

———

About the author. A year and a half ago, I learned about one shortcoming of our education system. We are simply not taught how to handle money. The school and the university turned out to be bad advisers in this matter. More precisely, none. Parents also have little to teach — they lived under a different economic system. Therefore, I took the issue of personal education into my own hands. Currently, I have been studying personal finance for a year and a half: starting from studying specialized business literature on the topic of Organization Finance, ending with books by Kiyosaki and Russian authors.

Now I have started to test my knowledge in practice. I promise to share my experience, thoughts and the most relevant extracts from the theory with readers on the pages of the Life Hacker. I promise that the articles will be vital and understandable.

If you do not agree with some of my thoughts or you have ideas for improving existing, as well as the topics of new articles, or if you want to get answers to financial questions, leave comments on the articles. We will discuss)

———

upd. During the collective discussion of the topic, new thoughts were born on how to calculate this question. The bottom line is that now we also take into account the fact that the money received as a result of investments is also depreciated by the amount of inflation.

As for the topic of this article, if we invest money at 7% / per annum with a monthly capitalization and inflation of 6.1% per annum (as indicated in the terms of the article), we will lose 7% if we do not invest money from under the mattress.