The company can work with the performer regardless of whether he has the status of self-employed or not. But this means different expenses and responsibilities for her.

In cooperation with a person without self-employed status, the organization becomes Letter of the Ministry of Finance of the Russian Federation dated July 21, 2017 No. 03-04-06/46733 "On Calculating, Withholding and Transferring Personal Income Tax to the Budget in Respect of Payments to Individuals (Not Registered as Individual Entrepreneurs) under Civil Law Contracts, as well as Payment of Insurance premiums" his tax agent and is obliged to The Tax Code of the Russian Federation, Article 420 "The object of taxation of insurance premiums" for him to transfer the personal income tax (13% rate) and insurance contributions to the Pension Fund (22%) and the CHI Fund (5.1%). Technically, the tax must be deducted from the fee, but usually the customer and the contractor agree on the amount on hand, and all other payments go on top of it. That is, for a company, a freelancer without self-employed status costs a fee plus 40.1%.

The self-employed pays the tax for himself. And the rate is lower — only 6%. Usually, the amount still falls on the shoulders of the employer — the fee increases by this percentage. But the difference between 6 and 40% is very impressive.

Therefore, cooperation with the self-employed looks attractive. But in order for everything to go smoothly, you need to make sure that the performer has this status. If it turns out that it is not, then the tax service will have claims The Tax Code of the Russian Federation, Article 123 "Failure by a tax agent to withhold and (or) transfer taxes" due to the fact that the company did not fulfill the duties of a tax agent.

And the status may not be for various reasons. For example, if a person simply lied because the company wrote in the conditions that the performer should be self-employed. Or he changed his mind and refused this tax regime, but did not tell the customer. Or broke the rules and lost the opportunity to be self-employed. Therefore, it is important to make sure that there will be no surprises.

There are two ways.

You will not oblige him with this at all, because you do not need to run and collect documents. The certificate is issued in the "My Tax" application literally in a couple of clicks and completely free of charge.

And thanks to the paper, you will be able to make sure that the self-employed really has such a status on the date of issue of the certificate. (This is what the sample looks like.)

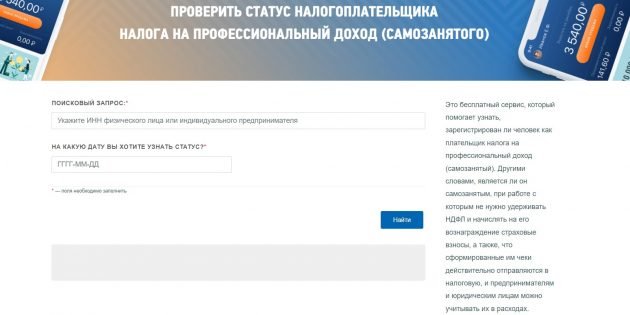

On the website of the Federal Tax Service there is a special service with which you can check the status of a person. To do this, you only need to know his INN.

If you do not know the TIN, but you know the passport data, you can also find out the taxpayer's number on the tax website.

There are additional ways to save the company from problems.

Specify in the papers the specific time within which the contractor must inform that he has ceased to be self-employed. And for violating this rule, provide, for example, a fine. Usually, the need to pay disciplines itself. But if it comes to recovery, at least it will be possible to compensate for the fine from the tax.

Their very presence confirms that the performer is self—employed. Otherwise, he would not have been able to issue a check in the "My Tax" application. So if he delays sending documents, this is a reason to be wary.